Here you can find answers to the most frequently asked questions regarding the different types of insurance coverage, the timeline of a personal injury lawsuit and what the three burdens of proof you need to prove in order to get compensation.

(The Injured Party’s Insurance)

Though it is often overlooked, there are many circumstances where a good Homeowners policy can provide additional coverage if you are injured from a third party's negligence. It also ensures that you protect your home, assets, and financial accounts if someone is injured on your property.

Like Homeowners Insurance, Renters Insurance can provide additional coverage for incidents involving third party conduct, dog bites, etc. Also important, Renters Insurance will protect you and your assets if someone is injured on your property.

Though it can be, and often is, expensive, a good health insurance policy will help you take care of your medical expenses while you focus on getting better. Though we can help you get the treatment you need, utilizing your health insurance coverage is often the best option.

Dental insurance is typically a minor expense added on with your health insurance policy. Dental care, like medical treatment, can be very expensive. Make sure you have sufficient coverage and a reasonable deductible so you are covered if you experience a dental-related injury.

There are several different types of disability insurance, and you should research all options available to you. Disability insurance will help you take care of yourself and your family if your injuries require you to miss work.

(The Liable Party’s Insurance)

In California, drivers are required to carry, at minimum, bodily injury liability coverage of $15,000 per person / $30,000 per accident and property damage liability coverage of $5,000. Still, as of 2015 over 15% of California drivers are uninsured. Even more carry just the minimum requirements. Though commercial policies typically have higher limits, a small percentage of drivers carry commercial coverage. It has never been more important to talk to your carrier about UM/UIM coverage.

Premises liability is the legal principle associated with personal injury matters involving an unsafe or defective condition on someone's property. Insurance companies offer premises liability insurance that insure against many of the risks associated with the ownership, use, or control of a property. Though coverage can be limited for a homeowner or renter's liability policy, commercial policies typically have higher limits.

Umbrella and excess insurance policies provide additional layers of coverage above primary insurance policies (i.e., commercial general liability policy or a personal/business auto policy). The difference between umbrella and excess coverage is that the umbrella can be used to cover some losses for which there is no insurance. The excess form usually only covers losses that are also covered by the other insurance policies in place at the time of the incident.

(The Liable Party’s Funds and Assets)

In some cases, a commercial entity or organization will establish its own "self-funded" insurance policy. This can significantly impact the adjuster's decision-making process regarding pre-trial or pre-arbitration settlement. Communication, strategy, and presentation is key when dealing with self-funded policies.

The availability of an insurance policy gives the injured party notice from the beginning that a damage recovery is possible. It can be very difficult, and sometimes prohibitively so, to pursue personal financial accounts. Having a knowledgeable attorney available to problem-solve the many issues associated with "judgment proof" parties is essential to you getting a recovery.

Like discovery into personal bank accounts, the judicial system is usually hesitant to allow early discovery into a third party's personal assets unless fraudulent activity is involved. You need someone who knows the alternatives and is capable of leveraging the possibility of a direct recovery against the insured party and their carrier. This requires aggressive and strategic representation throughout the pre-litigation and litigation process.

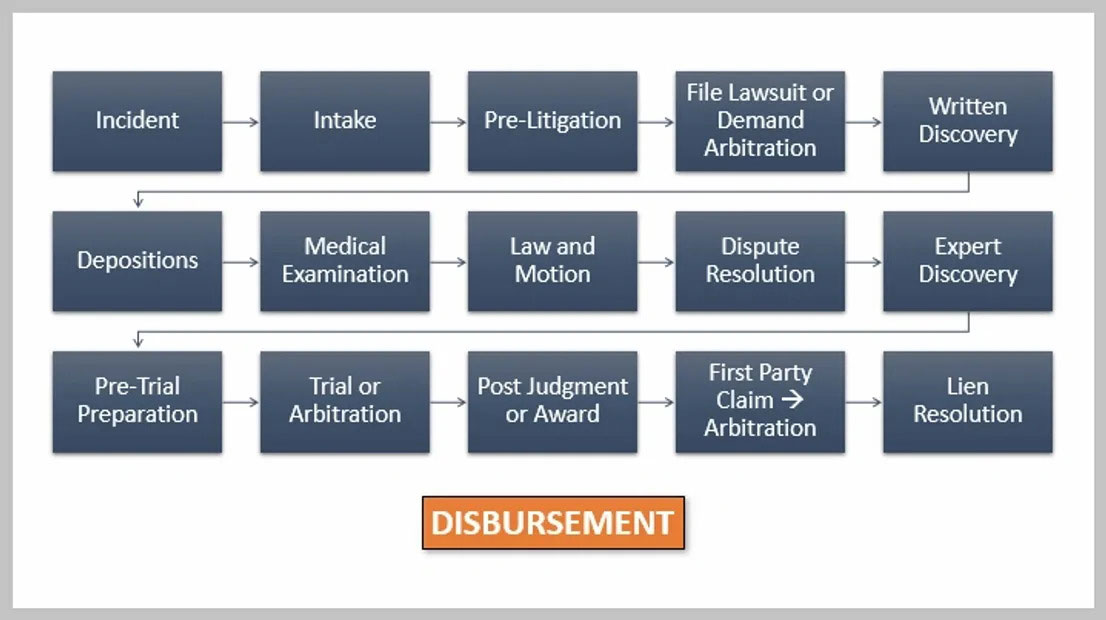

After an event involving injury, it is important for you or a family member to gather as much information regarding the incident as possible. This includes the other party's contact and insurance information, witness info, and documentation regarding your injury.

Many people who experience an injury do not want to speak with an attorney immediately, which is understandable. However, having an attorney involved from the outset lets the insurance carrier know you are represented and committed to enforcing your rights.

During the pre-litigation phase, we get to work by investigating the incident, tracking down copies of your medical records, and preparing an initial demand for the insurance carrier. Navigating the pre-litigation phase is essential to maximizing your recovery and building options for you later in the litigation.

For automobile collisions, unless the responsible party is uninsured you must first resolve the third party claim. This process is initiated by issuing a demand to the third party carrier or filing suit directly against the third party. On the other hand, if the third party is uninsured, the first step is to demand that your first party insurance carrier agree to arbitrate your claim.

Written discovery is typically your first opportunity to collect information directly from the adverse party. Cases can be won or lost based on how aggressively your attorney pursues written responses to pertinent discovery requests.

A deposition is the taking of an oral statement from a witness who is under oath, usually before trial. Depositions have two main purposes: (1) to find out what the witness knows, and (2) to preserve the witness' testimony for trial or arbitration. This process allows all parties the chance to collect all of the facts and relevant testimony before the matter is decided.

During litigation, insurance carriers will rarely rely on your medical records and treating physicians when deciding how to value your claim. Rather, it is common for the carrier to hire an "independent medical examiner" to conduct its own evaluation of your injury. This usually includes a medical examination and an IME report.

The efficient use of law and motion during the litigation phase is essential to the success of any personal injury matter, be it for gaining information, prevailing on issues in dispute, or making sure you try your case on your terms, not the insurance carrier's.

There are several opportunities during litigation to position or resolve your case prior to trial. These include demands, statutory offers, mediation, and ultimately, a mandatory settlement conference. Each can be used to push for a resolution or to collect valuable information from the carrier before trial or arbitration.

Expert discovery is the point in the case where both sides collect information and depose each other's liability, causation, and damage experts. This is a crucial part of the case, and one that directly impacts the possibility of a recovery at trial.

Though we are getting closer to trial, by now your attorney has already been preparing for trial for months. Witness preparation, document and deposition summation, drafting and presentation all begin to come together.

Almost to the finish line. Trial can take several days or it can span months. Each case is different and varies depending on the complexity of the action and each side's willingness to limit the issues in dispute.

You get a judgment or award. Now is the time where your attorney utilizes what they have done during discovery to hopefully increase your recovery even more.

Depending on the size of the first and third party policy limits, you may still be able to pursue first party insurance coverage if that coverage is in excess of the policy limit associated with the third party claim.

Though you pay a deductible and premiums for health insurance, your policy and state statutes allow the carrier to collect against your recovery. Our attorneys are experts at reducing these amounts, and we will continue to fight for you even after our fee is in hand.

The first thing that the injured party needs to prove is that the third party was liable for the incident (i.e., that the third party was negligent). Proving that the other party is liable for your injuries is essential to any personal injury claim, and it can be a very fact-intensive process. The ultimate question is whether the third party did (or didn't do) something that a reasonably careful person would not do (or would have done) in the same situation.

After liability, the next step is to prove that the third party's conduct or omission caused your injuries. It is very common for insurance carriers to reject or minimize claims due to pre-existing conditions or a failure to mitigate. Navigating these arguments requires a careful and thorough review of your medical records and an advanced understanding of your condition(s). Presentation and organization is key to telling the jury or arbitrator the right side of the story: your side.

Damages fall into two main categories: economic damages and non-economic damages. Economic damages include medical expenses, wage loss, and other "hard costs." Non-economic damages include, in part, your pain and suffering and emotional distress. Proving non-economic damages can be very difficult, especially with the many misconceptions of what non-economic damages are and how they are calculated. Having a personal injury attorney that is experienced in presenting damages is essential to your claim's success.

"*" indicates required fields